Trump Accounts for Newborns: What New Parents Need to Know

If you had a baby on or after January 1, 2025, the federal government wants to put $1,000 directly into a savings account for your child. No catch and no income limit. That's the headline behind Trump Accounts, a brand-new tax-advantaged savings vehicle created by the One Big Beautiful Bill Act. Here's exactly how it works and what you should do next.

What Is a Trump Account?

A Trump Account (officially called a Section 530A account) is a tax-deferred savings account established for children under 18. It was created by the One Big Beautiful Bill Act, signed into law in 2025, and accounts officially became available starting July 4, 2026.

Think of it as a hybrid between a traditional IRA and a custodial investment account. The money grows tax-deferred, meaning you pay no taxes on dividends or gains while the account compounds. After your child turns 18, the account transitions to traditional IRA rules, which means distributions are taxed as ordinary income and early withdrawals (before 59½) generally carry a 10% penalty, with exceptions for higher education expenses and first home purchases.

The government is not making this complicated. There's an official website at trumpaccounts.gov with more information that may be worth a read before opening an account.

Who Gets the Free $1,000?

The $1,000 pilot program contribution is available for children who meet all of the following:

Born between January 1, 2025, and December 31, 2028

U.S. citizen

Valid Social Security number

No prior pilot program contribution election has been filed for them

There's no income limit on eligibility for the $1,000 deposit, which is unusual for a federal benefit. Families at every income level qualify. Children born before 2025 can still open a Trump Account, but they don't get the $1,000 government seed contribution.

How to Open a Trump Account

You can open a Trump Account by filing IRS Form 4547 (Trump Account Election) with your 2025 tax return. Starting in mid-2026, you can also make the election directly online at form.trumpaccounts.gov.

Once the election is made, your child's account gets established and the $1,000 pilot deposit flows in. As of early 2026, more than 4 million children had already been signed up, with 1 million claiming the $1,000 pilot program contribution.

Contribution Limits and Who Can Contribute

The annual contribution limit is $5,000 total per child, from all sources combined. That $5,000 can come from parents, grandparents, family members, or employers.

One detail that stands out for business owners: employers can contribute up to $2,500 per year to an employee's Trump Account (or an employee's dependent's account) through a Trump Account Contribution Program (TACP) under a cafeteria plan. Those employer contributions do not count toward the employee's taxable income.

If you run an S-corp and want to offer this as a benefit to yourself as an employee-owner, that $2,500 employer contribution comes out pre-tax. It still counts against your child's $5,000 annual limit, so the remaining $2,500 can come from personal contributions.

One important clarification: individual contributions to a Trump Account are not tax-deductible, unlike a traditional IRA contribution. The tax benefit is entirely on the growth side.

Where the Money Gets Invested

Funds in Trump Accounts must be invested in low-cost U.S. equity index funds or ETFs that meet specific criteria:

Track an index of primarily U.S. companies (like the S&P 500)

Do not use leverage

Charge annual fees of no more than 0.10% of the account balance

Until the child turns 18, the money stays in these index funds and cannot be withdrawn (with very limited exceptions for death or rollover to an ABLE account). After age 18, the account owner can choose how to manage it, subject to traditional IRA distribution rules.

How Much Could a Trump Account Grow?

This is where things get interesting, and where it's worth being specific rather than letting the projections run wild.

I went ahead and ran a couple Monte-Carlo simulations to model out what return profiles really looked like depending on how these accounts are invested and how often parents contribute on behalf of their child. I utilized a large cap growth asset selection with no international equities (per the fund requirements of Trump Accounts) to get the asset simulation results listed below. This should give a more accurate projection than a simple interest calculation that doesn’t account for the variable nature of stock market returns from year to year.

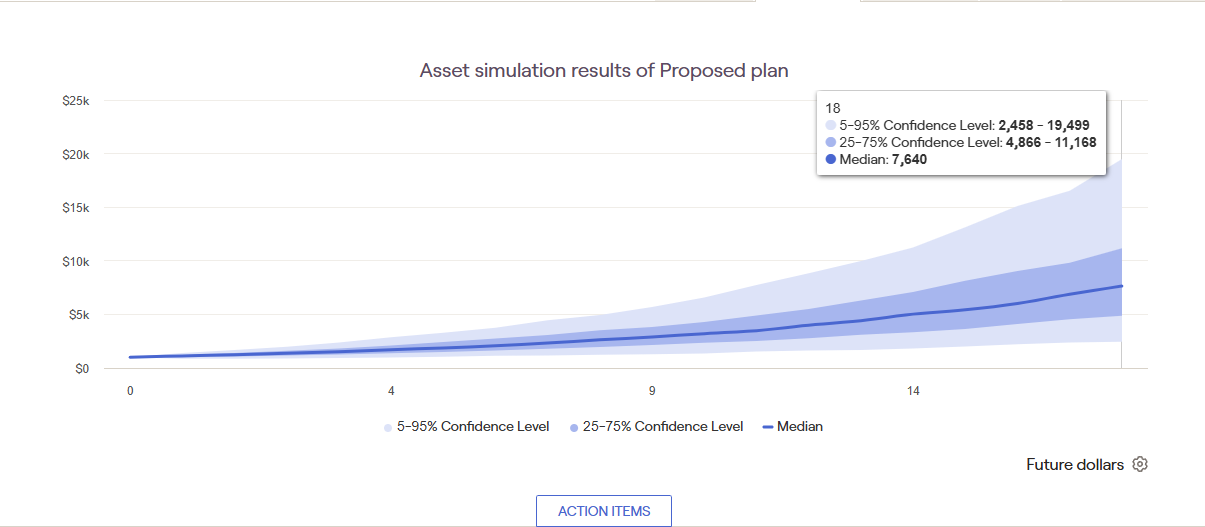

Scenario 1

Annual Contribution: $0

Assumed Asset Allocation: Large-Cap Growth

Value illustrated below is at Age 18

$1000 Seed-only deposit from the government

The $1,000 alone isn't life-changing money at age 18. What matters is whether you layer consistent contributions on top of it. Below is what a maximized trump account balance looks like from age 0-18 ($5000 contributed to the trump account every year while investing in a US Large-cap growth index portfolio.

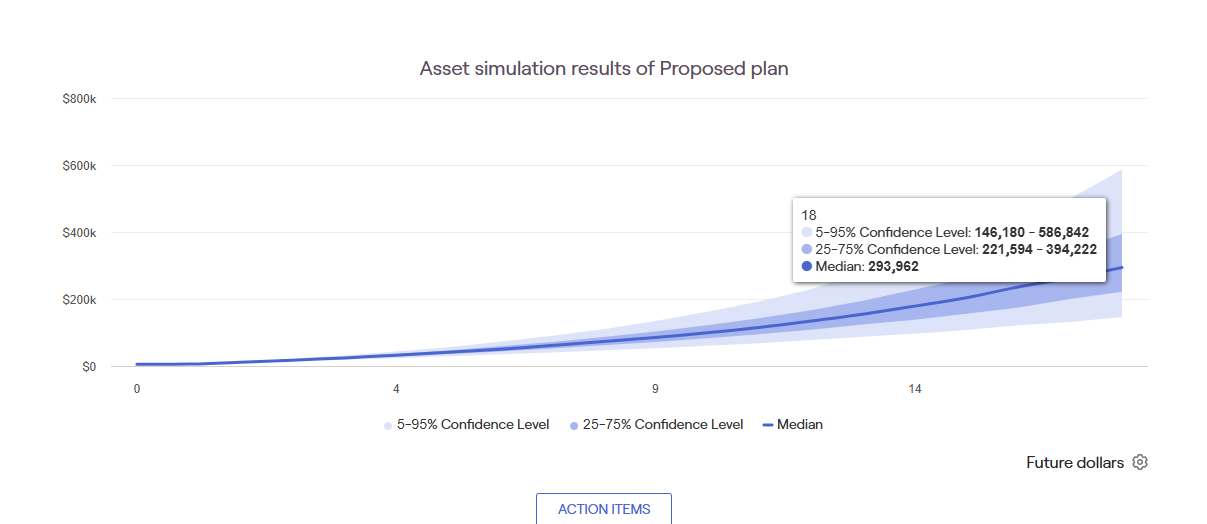

Scenario 2

Annual Contribution: $5,000

Assumed Asset Allocation: Large-Cap Growth

Value illustrated below is at Age 18

$5000 deposit years 0-18

Next, is the same setup as the projection above where contributions end at 18 and investments are allowed to grow until your child reaches 22. The idea behind this calculation is completing high school at 18 and then pausing contributions to the trump account while your child is a student finishing a 4 year degree or professional training program. There is a reasonable future where your child could have almost a half of a million dollars invested on their behalf by the time they are finishing their education as demonstrated below (given the above investing criteria and a consistent $5000 per year contributions from ages 0-18).

Scenario 3

Annual Contribution: $5,000

Assumed Asset Allocation: Large-Cap Growth

Value illustrated below is at Age 22

$5000 deposit years 0-18

How Trump Accounts Compare to Other Kids' Savings Options

Trump Accounts are not replacing 529 plans, UTMA accounts, or Roth IRAs for minors. They're a new option that works best alongside existing tools.

A few quick comparisons worth knowing:

Trump Account vs. 529: A 529 is purpose-built for education, with tax-free withdrawals for qualified education expenses. A Trump Account is broader but more restricted before age 18. If your primary goal is college funding, a 529 or a normal taxable brokerage account still wins on flexibility.

Trump Account vs. UTMA/UGMA: UTMA accounts have no contribution limits and no restrictions on withdrawals, but growth is taxable annually (the "kiddie tax" applies). Trump Accounts have a $5,000 cap but still grow tax-deferred.

Trump Account vs. Roth IRA for minors: A Roth IRA for a child requires earned income. A Trump Account has no earned income requirement, which makes it accessible from birth.

For most families, the answer isn't either/or. It's where does this fit in the broader picture, and how much can you realistically contribute across all of them.

What to Do Next

If your child was born in 2025 or 2026: File IRS Form 4547 with your 2025 return or claim the election online at trumpaccounts.gov. The $1,000 pilot deposit is available for eligible children, and the window runs through December 31, 2028.

If your child was born before 2025: You can still open a Trump Account, you just don't receive the $1,000 seed. Evaluate whether the tax-deferred growth is worth adding to your savings mix.

If you're a business owner: Talk to your financial advisor about whether establishing a Trump Account Contribution Program as an employer benefit makes sense, particularly if it can be run pre-tax through a cafeteria plan.

Start contributing something, even small. As demonstrated above, the math rewards consistency more than simply claiming the initial $1000 and “letting it ride”.

If you want to think through how a Trump Account fits into your broader financial plan for your family, including how it interacts with your S-corp, I work with clients on exactly this kind of planning at Alonso Financial Planning.

Frequently Asked Questions

Can I open a Trump Account for a baby born in 2024? Yes, children born before 2025 are eligible to have a Trump Account opened for them, as long as they're under 18 at the end of the calendar year the election is made and have a valid Social Security number. However, only children born between January 1, 2025, and December 31, 2028, qualify for the $1,000 pilot program deposit from the government.

What happens to a Trump Account when my child turns 18? Starting January 1 of the year your child turns 18, the account transitions to traditional IRA rules. Distributions become taxable as ordinary income, and withdrawals before age 59½ generally carry a 10% early withdrawal penalty, though exceptions exist for qualified education expenses and first home purchases (up to $10,000 lifetime). Your child can keep the money invested and let it continue growing tax-deferred.

Are Trump Account contributions tax-deductible? No. Contributions from individuals (parents, grandparents, etc.) are not deductible on your federal tax return. The primary tax benefit is deferred growth inside the account. Employer contributions through a qualified Trump Account Contribution Program (TACP) are excluded from the employee's taxable income, which is a different kind of tax advantage.

What if my child doesn't use the money for college or a home? Trump Accounts aren't restricted to specific uses after age 18. The account simply converts to traditional IRA rules, meaning your child can leave it invested and withdraw in retirement, subject to ordinary income tax at that point. Unlike a 529, there's no penalty for using the funds for non-education purposes after age 18, though early withdrawal before 59½ generally triggers the standard IRA 10% penalty (with exceptions).