Solo 401(k) vs. SEP-IRA: The Retirement Decision S-corp Owners Get Wrong

Many S-corp owners choose the SEP-IRA because it's simpler to open and someone told them the contribution limits were "basically the same." They're not. For a business generating $150,000 in profit, the difference between these two plans can easily exceed $24,000 in tax-deferred savings per year. That's the employee deferral in a Solo 401(k), and the SEP-IRA doesn't have one.

Understanding why requires a short detour into how S-corp income actually flows.

Your W-2 Wages, Not Your Distributions, Drive Everything

S-corp owners get paid two ways: W-2 wages as an employee of the corporation, and shareholder distributions from profits. The distributions are attractive because they aren't subject to self-employment tax. For retirement contribution purposes, only your W-2 wages count. That's not obvious, and a lot of owners find out at tax time when the math doesn't work the way they expected. Distributions are invisible to both plans.

This creates a scenario that plays out constantly. An S-corp owner earns $200,000 from the business, pays themselves $60,000 in W-2 wages to minimize payroll taxes, and takes the rest as distributions. Completely legal if that $60,000 is a fair wage given the work they do in their business. But their entire retirement contribution calculation is based on that $60,000, not $200,000. The plan that makes better use of that smaller W-2 base matters a great deal.

How the Two Plans Are Built Differently

A SEP-IRA is an employer-only plan. The corporation contributes up to 25% of your W-2 wages, with a 2026 cap of $72,000. That's it. No second contribution bucket, no employee portion.

A Solo 401(k) has two buckets:

Employer contribution: 25% of your W-2 wages (same as the SEP-IRA)

Employee deferral: Up to $24,500 in 2026, contributed as an employee, regardless of what the employer side produces

The employee deferral is what makes the comparison lopsided at most income levels. Both plans produce the same employer contribution from the same W-2 base. The Solo 401(k) then layers an additional $24,500 on top (or $32,500 for those ages 50-59 and 64+, and up to $35,750 for those ages 60-63 under the SECURE 2.0 catch-up rules effective 2026).

At modest W-2 levels, the SEP-IRA simply cannot close that gap.

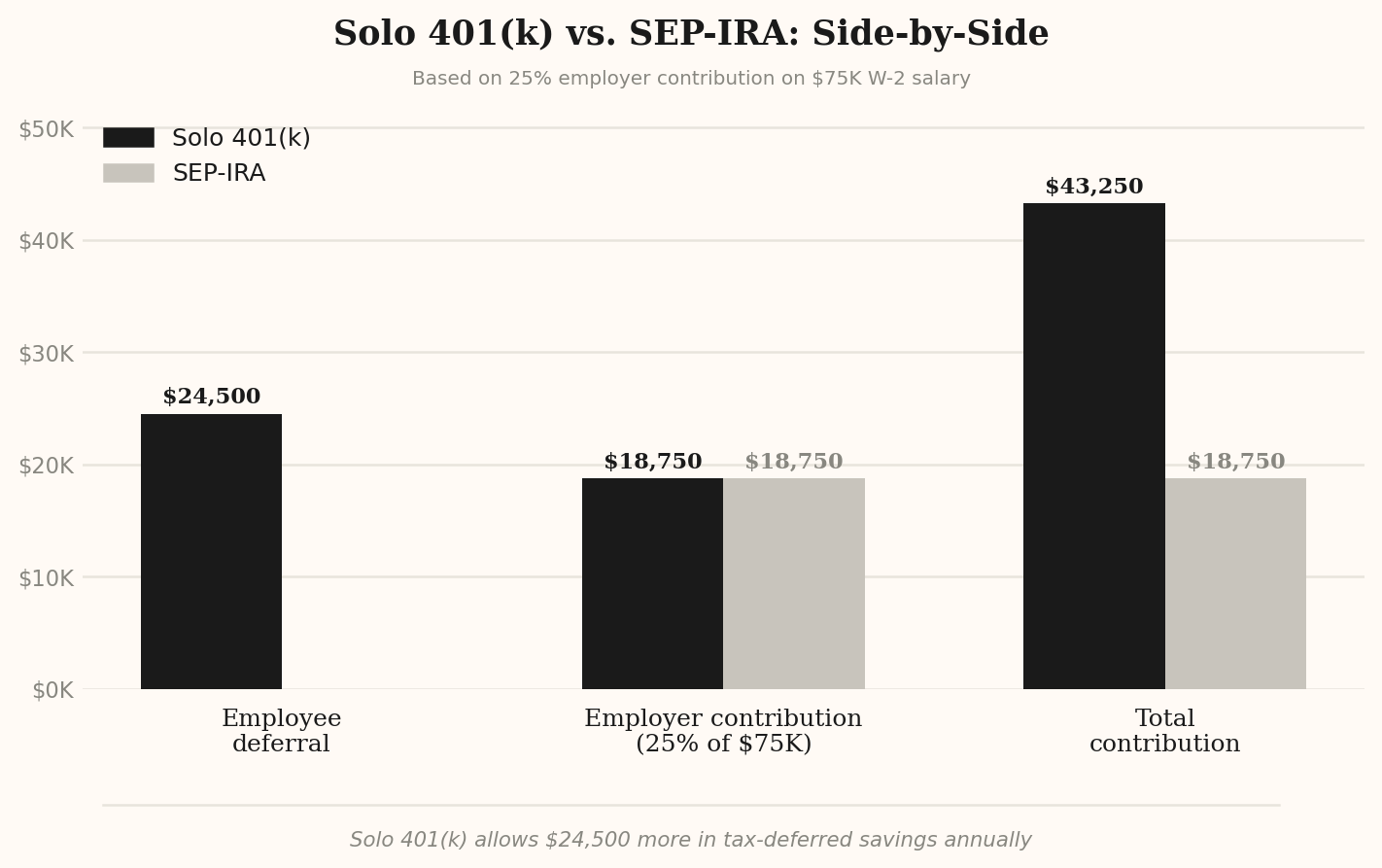

The $150K Profit Scenario: Side-by-Side

Assume your S-corp generates $150,000 in net profit for 2026. You pay yourself a W-2 salary (two examples follow), and the remainder flows to you as distributions.

Scenario A: $75,000 W-2 Wages

This is on the conservative end of "reasonable compensation" for a $150K profit business, though it may be appropriate depending on your industry, role, and hours worked.

At a 24% federal marginal rate, that $24,500 gap represents roughly $5,880 in deferred federal income tax for the year.

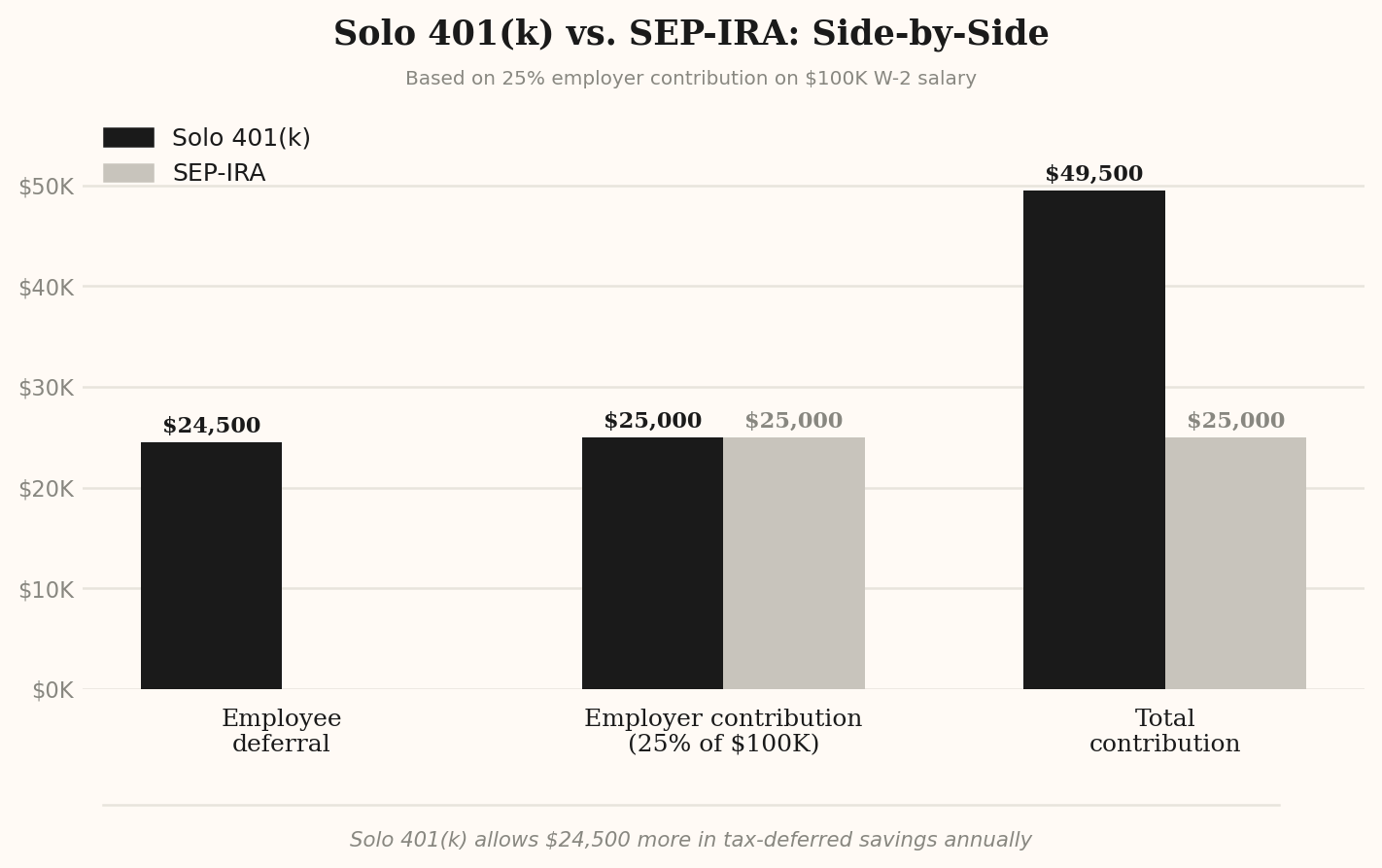

Scenario B: $100,000 W-2 Wages

Many advisors recommend a higher W-2 for businesses at this income level. The gap between the plans doesn't shrink.

Notice that as W-2 wages increase, the employer contribution grows equally for both plans. The Solo 401(k) stays ahead by exactly the employee deferral amount. The Solo 401(k) reaches its $72,000 total ceiling when W-2 wages hit approximately $190,000. Above that point, the Solo 401(k) is capped while the SEP-IRA continues to grow, and the gap fully closes only at W-2 wages of approximately $288,000, a level most S-corp owners at $150K in profit will never approach.

The Backdoor Roth Problem Nobody Mentions

There's a second reason financial planners consistently favor the Solo 401(k) over the SEP-IRA, and it has nothing to do with contribution limits.

High-income S-corp owners are typically phased out of making direct Roth IRA contributions. The workaround is the backdoor Roth: contribute to a traditional IRA, then convert it to Roth. It works cleanly if you have no pre-existing IRA balances. The catch is the pro-rata rule.

Under the pro-rata rule, the IRS treats all of your traditional IRA money as a single pool when you convert. If you're holding $68,000 in a SEP-IRA and you contribute $7,500 to a non-deductible traditional IRA to do a backdoor Roth conversion, only about 10% of your conversion comes out tax-free. The rest is taxable.

A Solo 401(k) sidesteps this entirely. The IRS does not include 401(k) plan balances in the pro-rata calculation. You can hold $200,000 in a Solo 401(k), contribute $7,500 to a non-deductible IRA, and convert the full $7,500 to Roth with no tax cost. Many Solo 401(k) plans also accept rollovers from existing SEP-IRAs, which lets owners clean up old IRA balances and restore their backdoor Roth access.

When the SEP-IRA Actually Makes Sense

To be fair: the SEP-IRA isn't a bad plan. It's just usually the wrong plan for solo S-corp owners.

The SEP-IRA has a genuine edge in two situations. First, if you have employees, a SEP-IRA requires you to contribute the same percentage of compensation for all eligible employees as you contribute for yourself. This uniform requirement can make a Solo 401(k) more attractive because it's designed for owner-only businesses. But if you have a simple setup and the administrative simplicity of the SEP-IRA outweighs the contribution difference in a given year, it works.

Second, the SEP-IRA has a later contribution deadline. You can fund a SEP-IRA up to your tax filing deadline including extensions. For S-corporations, that extended deadline is September 15. A Solo 401(k) must be established by December 31 of the year you want to make contributions, though you can still fund it until the tax filing deadline once established. If you're setting up a plan after year-end, a SEP-IRA is sometimes the only option.

For everyone else, especially a solo S-corp owner with no employees who is also doing backdoor Roth conversions, the Solo 401(k) wins on every dimension that matters.

What to Do Next

A few things worth keeping in mind:

Both plans calculate employer contributions the same way: 25% of W-2 wages, up to $72,000 for 2026. The SEP-IRA stops there. The Solo 401(k) adds an employee deferral of up to $24,500 on top of it.

Your W-2 wages are the foundation. Setting wages artificially low to minimize payroll taxes can unintentionally cap your retirement contributions. The two goals (tax minimization and retirement maximization) pull in opposite directions and need to be balanced deliberately.

The backdoor Roth issue is real. If you're doing backdoor Roth conversions or plan to, a SEP-IRA balance creates a tax drag through the pro-rata rule that a Solo 401(k) does not.

The Solo 401(k) has one meaningful administrative requirement: Once the plan exceeds $250,000, you must file IRS Form 5500-EZ annually. It's a one-page form. That's a small price for the contribution difference.

If you already have a SEP-IRA, you may be able to roll it into a Solo 401(k) to both consolidate accounts and restore clean backdoor Roth access. (Verify with a professional before moving forward)

If you're running an S-corp and you haven't stress-tested your retirement setup in a while, I work with S-corp business owners on exactly this kind of planning at Alonso Financial Planning. The right structure depends on your W-2, your profit level, and whether you're doing Roth strategies.

Frequently Asked Questions

Can I have both a SEP-IRA and a Solo 401(k) as an S-corp owner?

Generally, no. If your S-corp is your only source of self-employment income, you can't run a SEP-IRA and a Solo 401(k) simultaneously off the same business. The IRS treats them as competing plans for the same employer. You pick one structure per employer. If you have income from a separate, unrelated side business, the analysis gets more nuanced, but for a single S-corp owner, it's one or the other.

Does my S-corp distribution count toward retirement contributions?

No. Only W-2 wages paid through your S-corp payroll count toward Solo 401(k) or SEP-IRA contribution calculations. Shareholder distributions, while often a smart tax strategy for minimizing FICA exposure, are not considered earned income for retirement plan purposes. This is one of the most commonly misunderstood mechanics for S-corp owners who are new to the structure.

Is a Solo 401(k) worth the extra paperwork compared to a SEP-IRA?

For most solo S-corp owners, yes. The paperwork is modest. You set up the plan once, make contributions annually, and file Form 5500-EZ once the balance exceeds $250,000. The SEP-IRA is regarded as inferior in every material way for owner-only businesses, with the only counterargument being marginal setup convenience. Against an annual savings gap of $24,500 or more, that's a weak argument.

What happens if I set my W-2 too low to maximize my Solo 401(k)?

You cap your own contributions. Both the employee deferral ($24,500 in 2026) and the employer contribution (25% of W-2) require adequate W-2 wages to reach their potential. If your W-2 is $50,000, your employer contribution is only $12,500, for a $37,000 total (still better than the $12,500 a SEP-IRA would produce on the same wages, but short of what a higher W-2 would unlock). The "magic number" for W-2 wages to fully max out the Solo 401(k) at its 2026 ceiling is approximately $190,000. For most S-corp owners at $150K in profit, optimizing W-2 and plan selection together is where a conversation with a financial planner would be worth it.